Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

Recently, I came to a striking realization that has profoundly altered my perspective on earnings in the United States: a household bringing in $200,000 annually is no longer viewed as middle class. Rather, according to evolving financial aid calculations at prestigious colleges, incomes up to this level are now categorized as low income or even poor.

Having such designations as ‘poor’ or ‘low income’ attached to your earnings might not sit well at first glance. However, if top-tier universities are redefining $200,000 as the benchmark for poverty, it unexpectedly opens doors to substantial benefits for families. I am perfectly fine embracing this reclassification since it is merely a label. What truly matters is grasping the implications of these shifts for your household and leveraging them to thrive financially and personally.

For years, I have maintained that belonging to the middle class represents the most advantageous position in society. Middle-class individuals avoid the backlash of being labeled greedy, which often targets the wealthy, and they steer clear of the stereotypes of laziness sometimes unfairly applied to those with lower incomes. Politicians actively court this group because it forms the biggest voting demographic. Consequently, middle-class earners navigate life with reduced scrutiny and smoother interactions across various spheres.

There is undeniable strength in aligning with the majority demographic. Therefore, if your household income falls within the middle-class range, celebrate it! You enjoy widespread support and safeguards. Conversely, if you are pulling in a substantial salary, facing hefty tax burdens, and sacrificing family time through relentless work schedules, it is worth reevaluating if the sacrifices still justify the rewards.

When I transitioned from a lucrative career in finance to having no active income back in early 2012, I effectively became ‘poor’ by traditional measures. Paradoxically, this shift brought an immense sense of relief, as if a massive burden had been removed from my shoulders. I had reached a point of total burnout and yearned for respite. Escaping the cycle of toiling five months annually just to retain a portion of my earnings after grueling sixty-hour weeks felt truly emancipating.

In today’s landscape, I find myself pondering whether embracing a ‘low income’ status could surpass middle-class living in appeal. This is due to the broadening array of benefits available, diminished societal expectations, and the enhanced potential for a more balanced professional and personal life.

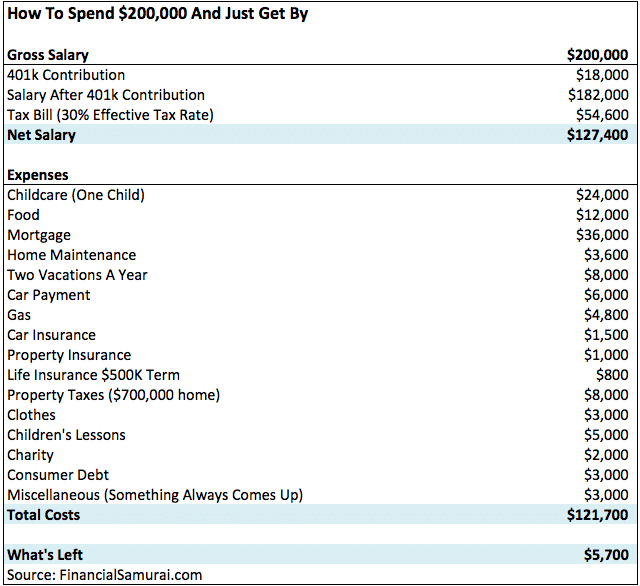

Once essential requirements like housing, food, and healthcare are met, additional earnings contribute only marginally to one’s overall sense of well-being and satisfaction. A $200,000 household income ought to sufficiently address the majority of family necessities. Moreover, in regions with lower living costs across the nation, $200,000 represents an exceptionally strong earning level that affords significant comfort and security.

On January 27, 2026, Yale University made headlines by declaring it would provide free tuition to prospective students hailing from families with annual earnings below $200,000. For households making under $100,000, Yale pledged to cover not just tuition but virtually all associated expenses, including room and board.

Keep in mind that approximately 96 percent of Yale applicants do not secure admission, making this policy a boon primarily for the select few who do gain entry and whose family incomes align with these criteria. In practical terms, Yale’s decision establishes that families earning up to $200,000 qualify as low-income or impoverished. Undoubtedly, Yale will factor in family size when adjusting these limits, recognizing that sustaining one child on $200,000 is considerably less challenging than providing for four.

Simultaneously, by covering all costs for families below $100,000, Yale is conveying that such households are deemed incapable of contributing even a nominal amount toward higher education. After parents have invested eighteen years in nurturing and housing their children, Yale steps in to assume responsibility for their young adult offspring’s living arrangements during four to five years of college. This level of support is remarkable.

It might seem counterintuitive to classify a six-figure salary as low-income or poor, yet I have authored multiple in-depth pieces featuring meticulous budgets that illustrate the struggles of advancing financially in high-cost metropolitan areas on $200,000 or even $300,000 annually. While some readers challenged my analyses, it is reassuring to witness elite academic institutions, which are intimately familiar with financial dynamics, validate that $200,000 does not stretch as far as commonly assumed for family sustenance.

Due to persistent inflation, a $200,000 household income no longer qualifies as affluent or solidly middle class, reshaping perceptions of financial status.

Despite the fact that a significant proportion of enrollees at Yale and fellow Ivy League schools originate from affluent backgrounds, this policy adjustment stands as a philanthropic move and savvy promotional strategy. The general public will likely be taken aback by the designation of $200,000 as low-income territory.

As avid followers of personal finance principles, we recognize that accumulated wealth and investment portfolios hold far greater importance than raw income for attaining true financial autonomy. Location plays a pivotal role too, determining the purchasing power of one’s salary.

Back in 2009, when I established this platform, I defined financial independence succinctly as generating sufficient passive income to handle everyday living costs. For instance, $25,000 in yearly passive earnings suffices for financial independence if your expenses match that level. Conversely, $300,000 in passive income falls short if annual spending hits $400,000.

The ultimate aim is to position your capital to generate returns autonomously, granting you the freedom to opt out of employment. Additionally, investment-derived income typically incurs lower tax rates compared to wage income, which is fitting since it has already undergone prior taxation.

Upon reviewing Yale’s policy reveal, I struggled to pinpoint exactly how family assets influence aid eligibility. Practices vary across institutions: some include primary residences in asset calculations, while others exempt them entirely.

Consider parents who faithfully contributed to a college savings plan over eighteen years, amassing funds to cover four full years of tuition while earning a modest $160,000 annually. Would their accepted child receive gratis tuition, or must they contribute regardless? Such dilemmas abound, especially given Yale’s ambiguous reference to typical assets alongside income brackets for aid qualification.

Recent data indicates that the proportion of students from the top 1% income bracket at elite colleges has risen to nearly 15% by 2026, highlighting ongoing disparities in access.

Here is a direct pull from Yale’s official statement, which provides sweeping assurances yet lacks granular details:

By elevating the income threshold for zero parental contribution to $100,000, close to half of all U.S. households with children aged six to seventeen would qualify for aid packages requiring no parental input on education costs. For families under $200,000, over 80 percent of American households could access Yale scholarships at minimum covering tuition expenses.

Currently, more than 1,000 Yale undergraduates benefit from zero-parent-share awards, with 56 percent of all undergrads eligible for need-based assistance. The typical grant for aided students this year surpasses the full annual tuition charge.

Yale further extends grants for necessities like winter apparel, international summer programs, and unforeseen economic difficulties.

I have prepared two thorough guides detailing strategies to finance college education and methods to unlock complimentary funds for higher learning. Should navigating these complexities prove daunting, professional consulting services exist to assist families in minimizing costs or optimizing aid packages.

If anyone can furnish precise information on asset treatment under these updated income guidelines, I would greatly appreciate it. Despite extensive searching, I found no such clarity. Financial aid administrators, your expertise would be invaluable!

One undeniable takeaway is that Yale and peer elite private universities prioritize income over assets in assessing financial need. This income-centric approach mirrors broader political rhetoric on taxation. Income is straightforward to quantify and communicate effectively. Yet, if we perpetually exchange our time for dollars, genuine liberation remains elusive.

This underscores why I advocate amassing substantial net worth as superior to endlessly pursuing salary increases. Progressive taxation escalates with income growth. Hitting federal marginal rates of 25 to 30 percent often prompts reflection on whether incremental effort merits the returns. Discontent with governmental priorities or local inefficiencies can further erode the drive to labor harder solely for higher tax contributions.

Households earning below $200,000 annually should feel optimistic about their prospects. This income level supports raising two children in comfort across most U.S. regions. Even in exorbitant locales like New York City or San Francisco, $150,000 to $200,000 sustains a family of four reasonably, provided private schooling is eschewed.

Should your children demonstrate extraordinary abilities, they might secure admission to premier universities with full financial coverage, dramatically easing your monetary load. That said, critics argue this policy serves as Yale’s performative gesture to bolster its image while preserving slots for full-paying enrollees.

![]()

While families agonize over the rigors of Ivy League admissions, universities themselves engage in cutthroat competition to recruit the brightest minds. With Yale extending free tuition up to $200,000 in family income, rival top institutions will invariably match or exceed this to stay in the race. Less selective private colleges must proffer even more alluring packages to lure elite applicants. This dynamic proves immensely beneficial for middle-class and lower-income households alike.

In the realm of higher education, endowment size dictates dominance. A stellar public university like The College of William and Mary, endowed with $1.5 billion, cannot rival Yale’s approximate $40 billion war chest. Ironically, wealth begets more wealth among these institutions. This pattern persists absent deliberate efforts to equalize opportunities, even temporarily.

Do you concur that $200,000 marks the contemporary cutoff for low-income status in lifestyle and family terms? Does $100,000 household income equate to poverty relative to $60,000+ annual private university tuition? And is the middle class indeed society’s premier socioeconomic tier?

To fully capitalize on college aid opportunities, initiate preparations during your child’s high school freshman year, or sooner if feasible. Institutions review family financial records spanning at least two years, occasionally extending further back.

Since departing my corporate role in 2012, I have depended on a robust free financial dashboard to oversee net worth, evaluate portfolio performance, and maintain transparent cash flows. Securing tuition-free college for your offspring could accelerate your path to retirement significantly.

This tool also offers a no-cost portfolio assessment for accounts exceeding $100,000 in investable assets. Gain profound insights into allocation strategies, risk profiles, and alignment with long-term objectives.

Modest optimizations implemented now can snowball into profound financial independence down the line. Families earning under these thresholds stand to reap expanded scholarships, fostering earlier financial security and reduced work years for parents. This policy evolution sparks vital dialogues on aid expansion, competitive offerings from additional colleges, and proactive financial strategizing.

As a parent, my focus remains laser-sharp on generating resources to fund education while safeguarding against future job market disruptions from AI and global shifts 15-18 years hence. Such announcements, paired with projections of escalating institutional aid, signal positive trajectories for family finances.

Location profoundly influences affluence perceptions: $200,000 affords luxury in affordable Texas towns with prevalent sub-$200,000 homes, attainable via dual earners or overtime in professions like medicine, law, or trades. Yet in globally recognized metropolises like NYC, LA, or Chicago, the same sum yields far less opulence, underscoring geographic variances in income value.

Elite universities’ finance teams acknowledge these pressures, prompting generous tuition waivers for qualifiers. This recalibration validates budgetary realities in expensive locales, where $200,000-$300,000 barely sustains middle-class aspirations amid soaring housing, education, and living costs. By de-emphasizing assets and spotlighting income, policies empower families to retain savings while accessing aid, though ambiguities persist around home equity or 529 balances.

Progressive tax structures and societal dynamics further incentivize net worth accumulation over income escalation. Families below $200,000 enjoy manageable lifestyles nationwide, with gifted children potentially unlocking elite education gratis. Competition among schools amplifies these gains, though endowments entrench advantages for the wealthiest institutions.