Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

One key factor behind my enduring support for Fundrise as a long-term advocate and partner stems from the company’s commitment to pioneering new approaches in investing. Established in 2012, just after the JOBS Act expanded opportunities for everyday investors to participate in private markets, Fundrise has continuously sought innovative methods to make high-caliber institutional investments accessible to a broader audience.

The platform has introduced a range of diversified private real estate offerings, such as the Heartland and Income funds, and has ventured into the realm of venture capital with the creation of the Innovation Fund. This progression has allowed Fundrise to enter territories traditionally dominated by major institutions and individuals with substantial wealth.

Thus, when an announcement arrived from Fundrise detailing intentions to take the Innovation Fund public on the New York Stock Exchange under the ticker symbol VCX, it immediately captured my attention and sparked considerable interest.

Personally, I maintain a traditional perspective on investment strategies. If a particular approach is functioning effectively, I hesitate to alter it unnecessarily. I first committed funds to the Innovation Fund back in 2023, and currently, my holdings exceed $700,000 spread across three separate accounts. My strategy involves maintaining these positions for the coming 5 to 10 years, capitalizing on the ongoing surge in artificial intelligence, with a primary focus on securing my children’s financial future.

Below, I outline my preliminary analysis regarding the prospective NYSE listing of the Innovation Fund, formulated after a full day of reviewing and reflecting on the development. I intend to revise this article as additional details emerge and my perspectives evolve further.

Throughout more than 15 years of engaging with conventional venture capital funds, I have grown accustomed to the reality of virtually no liquidity for extended periods. When directing capital into venture opportunities, which typically constitute around 20% of my total investable assets, I prepare mentally for a horizon of at least a decade before any returns might materialize.

The remaining 80% of my portfolio is structured to offer flexibility and access to cash when required or when compelling alternatives present themselves. This includes equities, fixed-income securities, and even digital currencies, all of which can be liquidated relatively swiftly. In stark contrast, venture capital embodies patient capital, designed for enduring commitment over rapid turnover.

Fundrise has already implemented quarterly redemption options for the Innovation Fund, which stands out as particularly accommodating within the venture capital landscape. However, sustaining this level of liquidity incurs certain expenses, a nuance I initially overlooked until a conversation with Ben Miller, the Chief Executive Officer of Fundrise, brought it into sharper focus.

In order to fulfill quarterly withdrawal demands, approximately 30% of the Innovation Fund’s assets have been directed toward more liquid, conservative instruments like money market accounts and corporate debt securities. While these holdings ensure stability and ready cash availability, they simultaneously temper the fund’s overall performance, particularly amid robust market upswings.

For instance, during 2025, the Innovation Fund achieved an impressive return of approximately 43.5%, propelled by standout contributions from key investments including OpenAI, Anthropic, Anduril, and Databricks. Comparatively, money market funds yielded around 4%, and corporate bonds hovered near 6%.

With 30% of the portfolio generating a blended yield nearer to 5%, this allocation exerts a notable downward pressure on results in bullish environments, akin to maintaining excessive cash reserves in a portfolio experiencing sharp appreciation. Moreover, in periods of strong performance, redemption requests were minimal, as participants preferred to remain invested and frequently increased their stakes.

This context underscores the appeal of a potential public listing on the NYSE for the Innovation Fund.

Should the fund achieve public status, the requirement to maintain a substantial portion in low-yield liquid assets could diminish considerably. Market mechanisms would supply the necessary liquidity, relieving pressure on the fund’s internal resources.

Employing basic preliminary calculations, reallocating that 30% from conservative holdings into the core portfolio alongside other assets could have elevated returns to nearly 60%, rather than the observed 43.5%. Essentially, the low-risk segment’s 5% return imposed a 13.5% penalty on overall outcomes. This represents a substantial implicit cost for extending liquidity to investors who, during market strength, rarely exercised it.

Naturally, market trajectories are rarely linear. Downturns and prolonged bear phases are unavoidable, particularly in sectors characterized by elevated valuations such as artificial intelligence. During such declines, investor behavior often shifts toward panic selling at lows after purchasing at highs.

For a private fund extending quarterly liquidity, a sharp correction in AI valuations might trigger overwhelming redemption volumes that exceed immediate fulfillment capacity, potentially necessitating temporary restrictions on outflows. Such measures breed dissatisfaction and complicate operations significantly.

A publicly traded fund navigates these challenges through price discovery via exchange trading. In times of heavy selling pressure, share prices naturally adjust to equilibrate supply and demand. Participants then face a deliberate choice: liquidate at reduced valuations or persevere with conviction in the portfolio’s foundational enterprises.

Fundrise, operational for about 14 years, presently oversees more than $3 billion in assets under management. Although the commercial real estate sector has encountered turbulence since the Federal Reserve’s aggressive rate hikes commencing in 2022, these issues appear largely temporary and sector-specific, not indicative of deeper operational or reputational flaws. Optimism persists that the commercial real estate cycle has begun to stabilize.

Securing an NYSE listing for the Innovation Fund would markedly bolster Fundrise’s standing and reputation within the investment community. Achieving such a milestone demands rigorous examinations by legal experts, investment bankers, independent auditors, and regulatory bodies, all entailing considerable time and financial outlay.

This process mirrors admission to a prestigious academic institution, conveying elevated standards of oversight, disclosure, institutional validation, and professionalism. Consequently, this could instill heightened trust among investors, fostering inflows of capital that in turn facilitate pursuit of even more attractive opportunities.

Admittedly, public status offers no ironclad assurance of triumph; mismanaged listed funds persist in the market. Nonetheless, the NYSE designation broadly projects Fundrise’s resolve, resilience, and dedication to sustained operations.

For emerging companies pursuing funding, an investor’s reputation carries substantial weight. Entrepreneurs assess backers not merely by financial resources—which abound in abundance—but by proven histories, expansive networks, and capacity to propel enterprise expansion.

Boasting a community exceeding 380,000 investors, Fundrise possesses a unparalleled distribution network seldom rivaled by conventional venture outfits. Its portfolio enterprises benefit from heightened visibility, prospective clientele, and enhanced legitimacy through mere affiliation.

These advantages have been highlighted in prior discussions with Ben Miller, Fundrise’s founder and CEO, particularly regarding collaborations like that with Ramp, which spurred substantial user growth via mutual promotion. Ramp’s leadership informed Ben that the initiative ranked among their most effective marketing efforts. Subsequently, Ramp surpassed BREX—its primary rival that launched two years prior—and culminated in an acquisition by Capital One.

As a stakeholder in the Innovation Fund, my foremost interest lies in the triumph of its holdings. I exemplify how individual investors can amplify exposure for these ventures, a capability shared by countless others within the Fundrise ecosystem.

Contrast this with elite venture firms such as Sequoia, renowned for stellar pedigrees and talent yet constrained to institutional allotments, privileged networks, and select founders. They lack the immediate reach to vast arrays of enthusiastic retail participants that Fundrise commands effortlessly.

Furthermore, Fundrise operates as a private entity actively utilizing and validating products from its portfolio. For nascent firms weighing investor options, this blend of funding, platform leverage, and hands-on expertise proves irresistibly persuasive.

An NYSE listing would amplify this narrative’s legitimacy even further.

Prior to delving deeper, it proves essential to delineate net asset value, or NAV, within this framework.

NAV signifies the per-share worth of the fund’s constituent assets net of obligations. Put plainly, it equates to the appraised total value of the Innovation Fund’s holdings—encompassing companies and other assets—divided by outstanding shares. In private structures, transactions occur proximate to NAV.

Upon public listing, market dynamics introduce a parallel influence: the interplay of buyer and seller interest in the shares themselves.

NAV persists as a function of portfolio performance and asset appraisals, yet the observable trading price may diverge from NAV based on prevailing sentiment, liquidity appetites, and share availability. This variance manifests as a premium or discount to NAV.

Empirical patterns among closed-end funds, notably those anchored in illiquid assets like real estate, frequently reveal discounts to NAV ranging from 5% to 10%. These arise from pragmatic considerations including liquidity demands, appraisal ambiguities, doubts regarding stewardship, or preferences for direct asset ownership over fund wrappers.

Conversely, limited supply can invert this pattern dramatically.

Should enthusiasm for specific private market exposures outstrip available shares, trading prices may substantially exceed NAV. Here, price fluctuations stem more from public market imbalances than shifts in underlying valuations.

Such phenomena already materialize in select market niches. Certain exchange-traded instruments concentrating on elusive private equities have commanded persistent premiums surpassing their NAVs.

For the Innovation Fund, this introduces a novel dimension for consideration. Future returns would derive not exclusively from portfolio efficacy but also from contemporaneous market valuations of access to these assets.

Fundamentally, asset values dictate NAV, while market fervor governs whether shares transact at premiums, discounts, or parity thereto. The relative inaccessibility of portfolio constituents could propel premiums higher.

From my vantage as a horizon-focused investor, I anticipate trading near NAV, perhaps with a slight discount. Yet, given the fund’s exclusive private holdings and constrained public float—potentially 8% or below—a demand-driven premium remains feasible, at least intermittently.

This market overlay introduces price swings but concurrently unlocks potential accretive dynamics absent in private formats.

Established examples affirm the viability of listed funds commanding NAV premiums. A prominent case is DXYZ, the Destiny Tech100 Inc. fund, which has fluctuated between 200% and 350% premiums to its NAV. As of November 2025, NAV approximated $7 per share, presumably elevated since.

With SpaceX comprising nearly half the portfolio, DXYZ exemplifies voracious appetite for restricted-access proxies like SpaceX equity. Participants willingly remit hefty markups for accessibility, rarity, and anticipated growth trajectories.

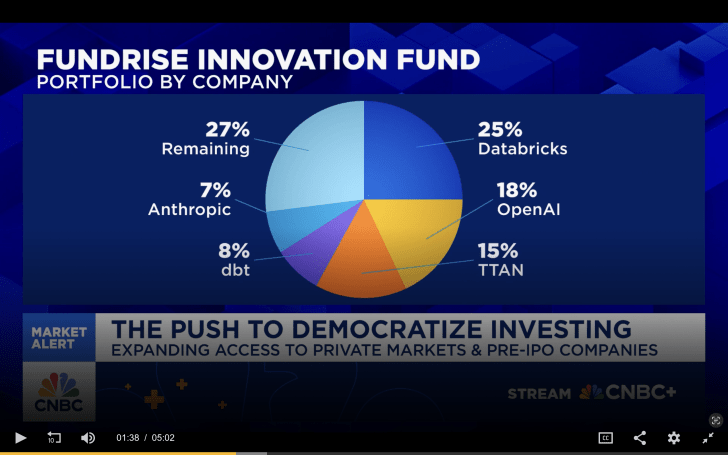

Discerning observers might ponder parallels for a listed Innovation Fund. Per a third-quarter 2025 CNBC overview, Databricks, OpenAI, and Anthropic collectively represented about 50% of holdings, complemented by premium private names including Canva, Anduril, Ramp, and likely SpaceX.

The Innovation Fund arguably presents a more balanced array of private growth entities, mitigating single-name risks relative to DXYZ. This profile plausibly supports premium trading, especially amid barriers to direct investment in these firms.

ServiceTitan, now listed as TTAN and comprising under 2% of assets (contrary to outdated graphics showing 15%), underscores the portfolio’s emphasis on private opportunities over public ones.

Premiums, while conceivable, warrant treatment as supplementary rather than assured. Sentiment proves fickle, prone to contraction amid corrections or rate pressures, irrespective of portfolio vigor. Diversification tempers extremes relative to SpaceX-centric vehicles.

NAV ranging from $6.50 to $9, yet trading at premiums amid elevated fluctuations. Nonetheless, the overlaid trend (depicted by white line) trends upward.

To ground expectations, consider a scenario assigning 50% probability to a 10% NAV discount, 20% to parity, and 30% to a 50% premium (eschewing DXYZ-like extremes). Under these weights, a pre-listing $100,000 outlay anticipates $110,000 valuation.

This profile of skewed upside aligns with my tolerance for extended commitments. Readers are encouraged to model varied inputs for personalized insights.

My horizon spans at least five years, preferably ten, extending to my children’s college completion in roughly 16 years, buffering against AI-disrupted employment landscapes. Compounding favors patience, rendering post-listing lockups inconsequential.

Tax considerations demand outsized premiums to prompt divestment. Projecting 20% annual compounding over five years yields approximately 150% appreciation via retention alone.

Exiting justifies itself only at substantial premiums with superior redeployment prospects. Absent that, leveraging assets while deferring taxes mirrors strategies of affluent holders.

An extraordinary 100% premium post-lockup might prompt trimming 25% of holdings to harvest gains, preserving 75% for continuation—equating to ~$700,000 uplift on my current stake purely from listing effects. Partial realization harmonizes caution with optimism.

Discount scenarios elicit steadfast holding, anticipating convergence as market familiarity grows.

Primary dashboard for my Fundrise venture investments, featuring over $200,000 designated for family, plus my spouse’s $100,000+ allocation.

Drawing from a decade-plus nurturing Financial Samurai since 2009, I appreciate the rigors of scaling enterprises and cultivating brands. Progress can accelerate or stall amid adversities, an inherent facet of substantive endeavors.

Pursuing an NYSE listing for the Innovation Fund advances Fundrise’s trajectory toward amplified disclosure, seamless liquidity, and fortified brand resilience. Over time, this may elevate deal flow quality, aligning incentives for platform and participants alike.

Compensation structures retain appeal: accessing elite private growth without 20% performance allocations remains exceptional. Contrast with one of my closed-end venture commitments levying 3% management plus 35% profits; Fundrise’s 2.5% fee sans carry shines brightly.

The paramount hurdle for stakeholders, including myself, involves maintaining resolve. Enhanced liquidity tempts impulsive exits in slumps, rationalized by persuasive rationales. My dual-sided analyses equip me to navigate biases.

AI private markets will inevitably correct. True mettle emerges in enduring turbulence or opportunistically accumulating undervalued positions, predicated on AI’s multi-decadal arc.

In summation, anticipation surrounds the listing vote. With a mere $10 entry threshold, Innovation Fund participation demands minimal barriers. Absent listing success, the current framework suffices; novel private growth vehicles from Fundrise will merit scrutiny.