Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

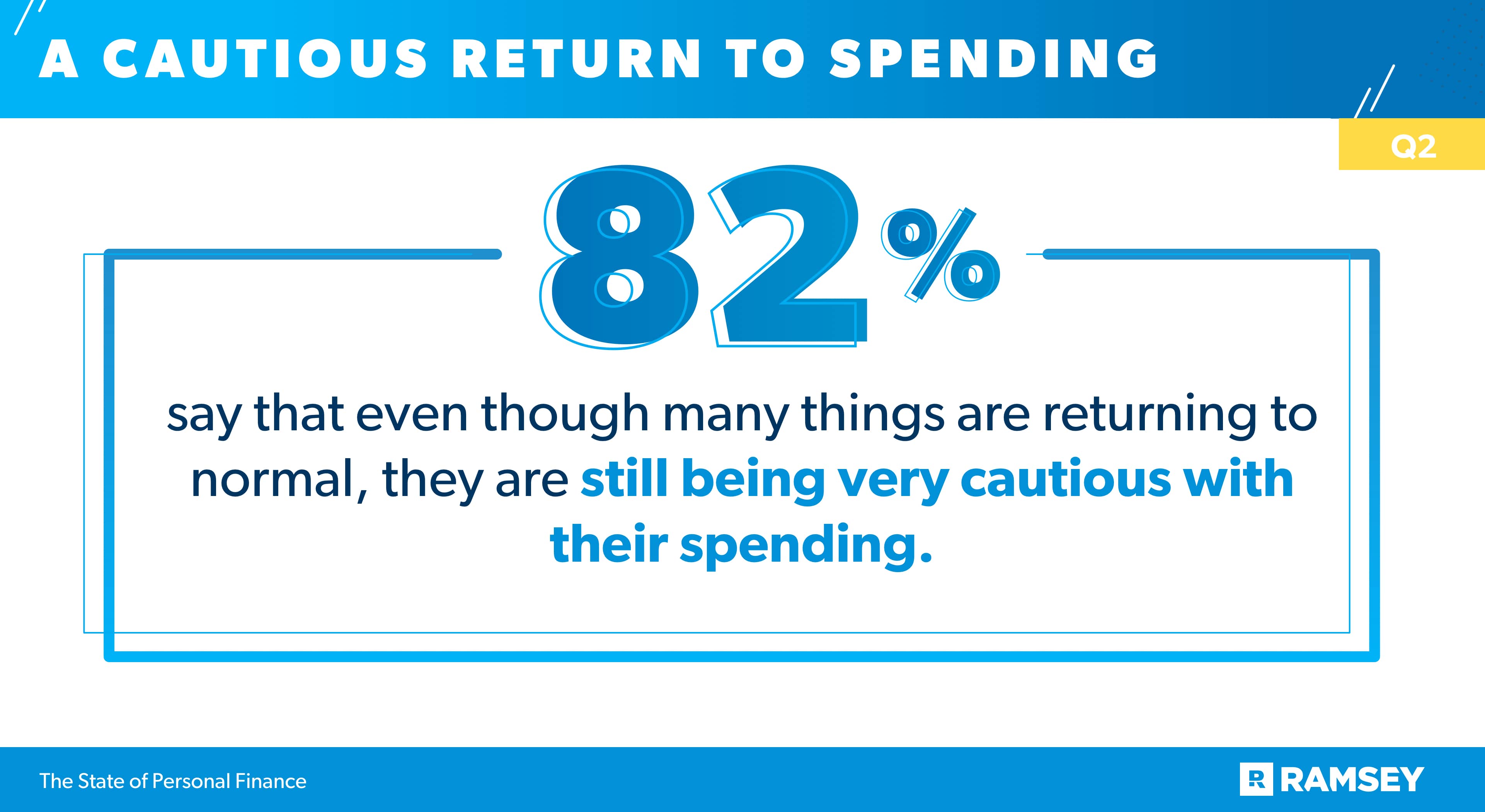

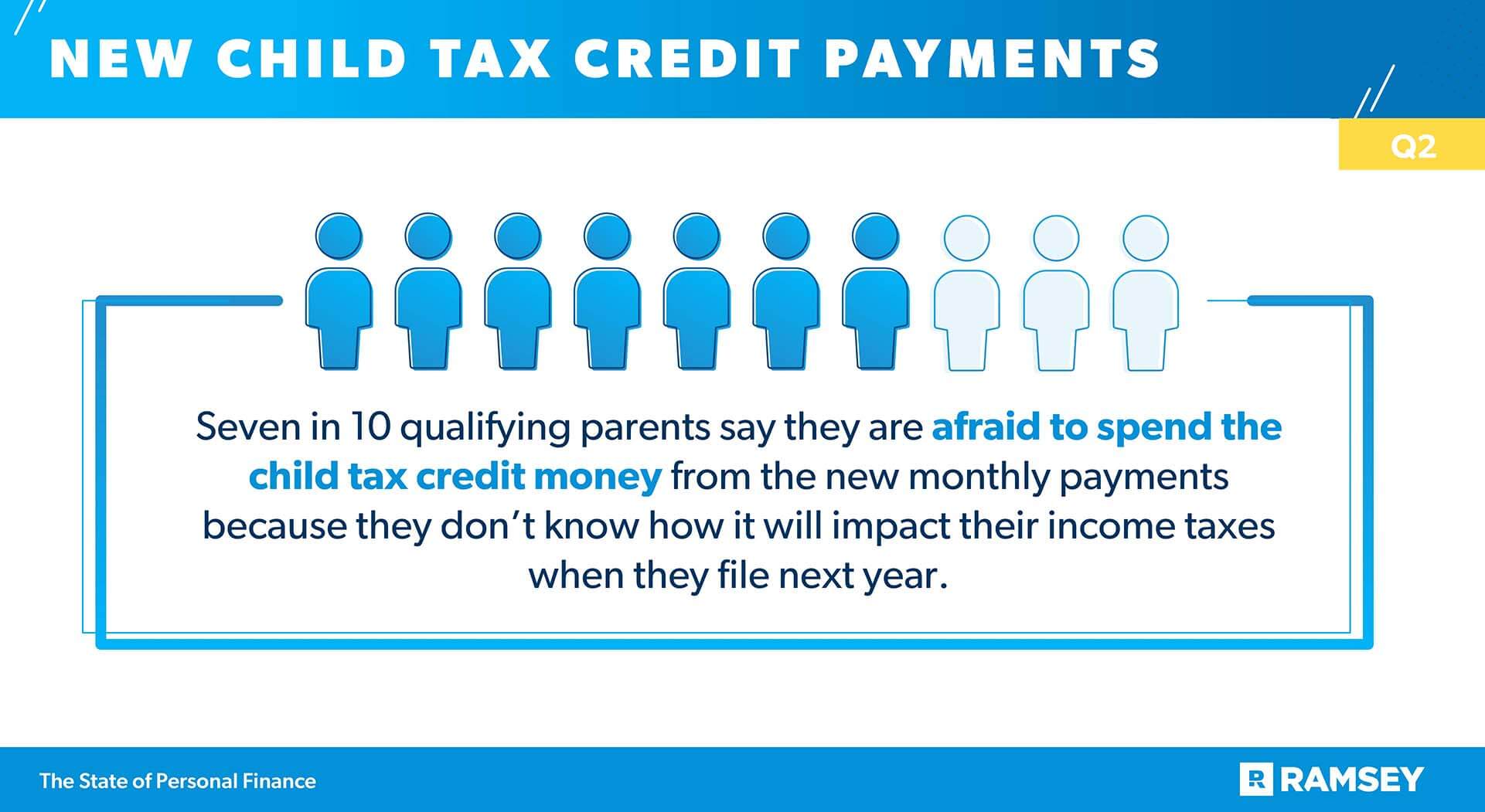

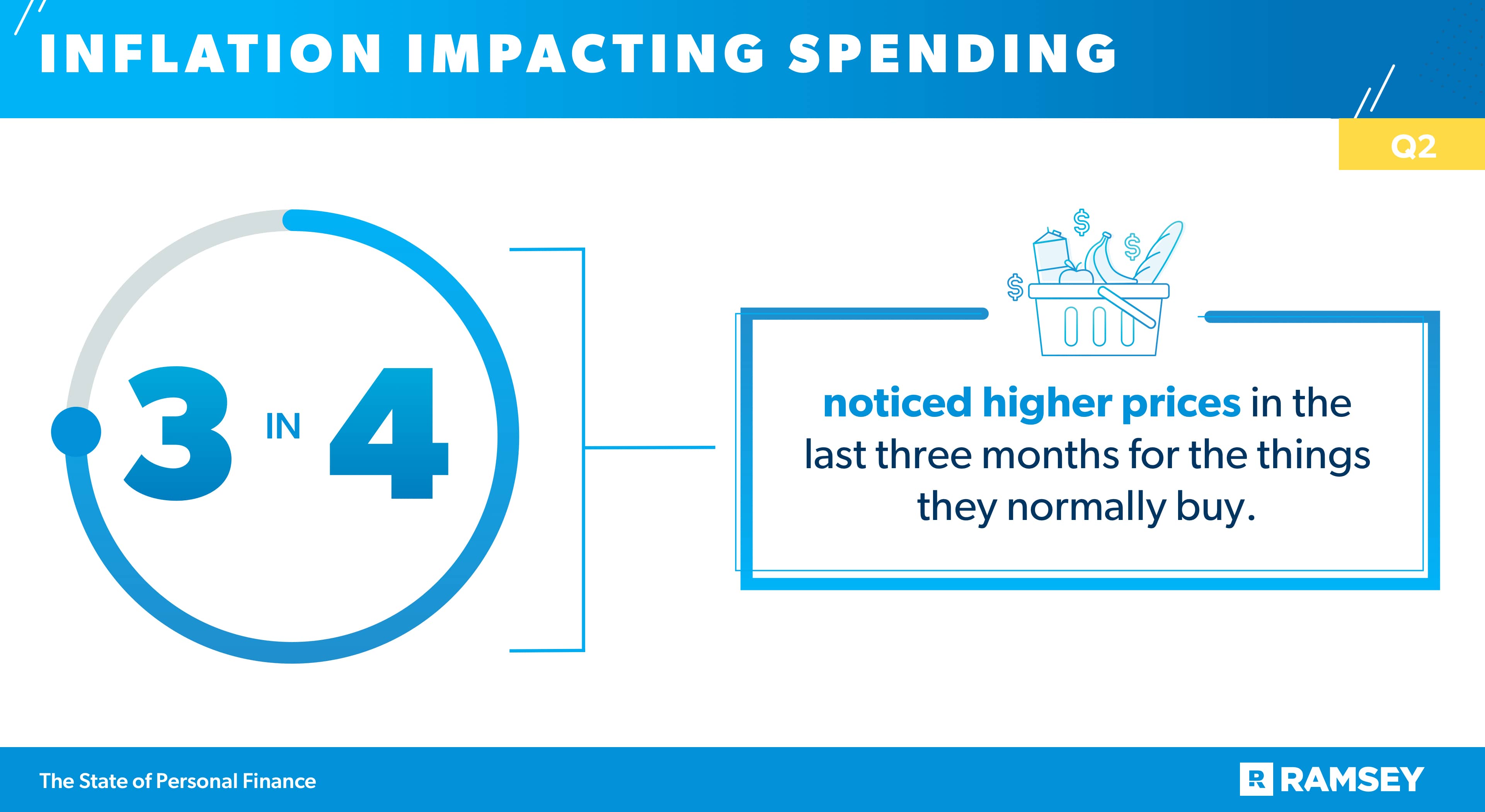

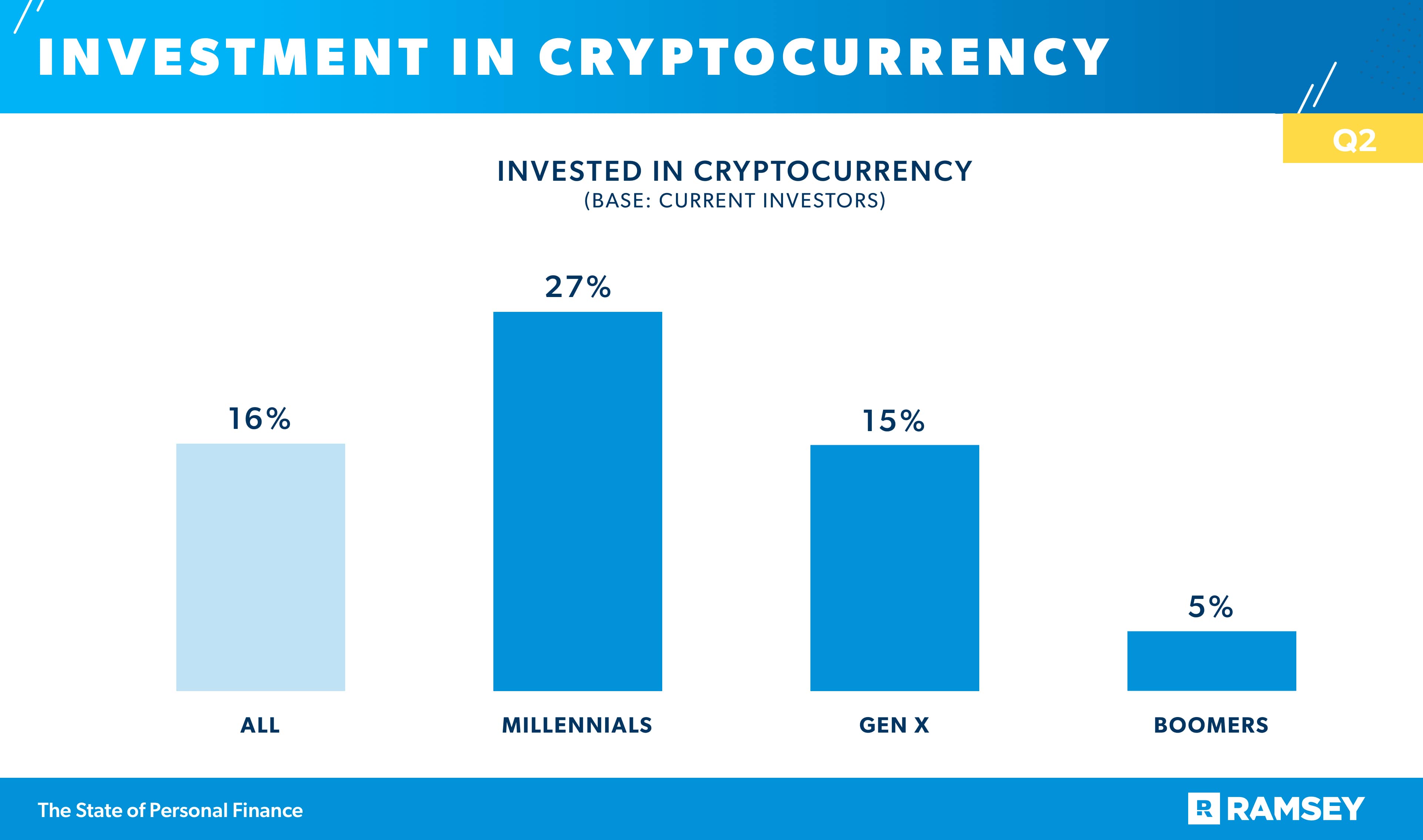

Almost six out of every ten individuals indicate that, with numerous regions of the nation resuming activities similar to those before the pandemic, they feel prepared to allocate funds toward personal indulgences and rewards. A substantial 82% of respondents affirm that, despite the gradual return to everyday routines across various sectors, they continue to exercise significant restraint and carefulness in their expenditure decisions. Among eligible parents, 70% express apprehension about utilizing the newly introduced monthly child tax credit disbursements, citing uncertainty regarding potential effects on their upcoming income tax obligations. Three-quarters of participants have observed elevated costs over the past three months for everyday purchased items. Sixty percent of individuals who recently acquired homes report having exceeded the listed price for their property transactions. Sixteen percent of current investors have allocated capital into various cryptocurrencies. Furthermore, 41% of married individuals report experiencing frequent disagreements with their partners during financial discussions.

As the U.S. economy shows signs of recovery and various restrictions from the pandemic era begin to lift during the summer months, fresh research reveals a sense of guarded optimism among the populace concerning their monetary circumstances. A considerable number of citizens perceive their financial positions as improved relative to the same period in the previous year, yet they maintain a prudent approach prior to significantly boosting their outlays. The most recent quarterly installment of Ramsey Solutions’ State of Personal Finance analysis explores these dynamics in depth, alongside examining the ramifications of rising inflation on domestic budgets, ambiguities surrounding the new child tax credit distributions, and apprehensions linked to the intensely competitive real estate sector favoring sellers.

A significant portion of the American population senses that economic conditions are stabilizing, and following an extended period marked by unpredictability and fiscal conservatism, shoppers are poised to gradually revert to accustomed purchasing behaviors with measured steps. Close to 60% express readiness to invest in self-rewards now that pre-pandemic lifestyles are reemerging in many areas. Indeed, 63% have outlined plans for substantial or high-value acquisitions within the forthcoming quarter. It comes as no surprise that seasonal vacations lead the roster of anticipated major expenditures, with over a quarter (27%) intending to budget for trips in the near term. This enthusiasm is particularly pronounced among Millennials, as 45% of those scheduling summer getaways anticipate higher expenditures this year compared to the prior one. In contrast, merely one-third of Generation X members and 29% of Baby Boomers expect to increase their vacation budgets beyond last year’s levels.

Nevertheless, the financial wisdom acquired amid the COVID-19 crisis remains vivid in the minds of many. Numerous individuals who curtailed discretionary spending and bolstered their savings reserves to weather the storm report that these practices will persist indefinitely. Specifically, three-quarters intend to retain certain pandemic-induced modifications to their spending routines on a long-term basis. Moreover, 82% emphasize their ongoing vigilance in managing expenditures, even as normalcy resumes in multiple facets of life.

This reluctance to loosen the purse strings extends into various other monetary choices. Recent legislative adjustments to the child tax credit enable qualifying parents to obtain half of their entitled amount via monthly installments from July through December this year. These installments can reach up to $250 monthly for each eligible child aged 6 to 17, and $300 for those under 6 years old. The remaining portion is redeemable upon submitting 2021 tax returns in 2022. However, a large majority of eligible parents exhibit hesitation in deploying these funds immediately.

Seventy percent of qualifying parents voice fears about spending these monthly child tax credit allotments due to unclear implications for their forthcoming tax liabilities. The current quarter’s investigation reveals that just half of these parents claim a solid grasp of how this program influences their overall tax scenario. Comprehension levels dip further among lower-income households: nearly 40% of those earning under $50,000 annually, 44% in the $50,000–$99,999 bracket, and 60% above $100,000 report clear understanding of the tax repercussions from these payments.

Paradoxically, despite greater awareness, higher-income families display even stronger reticence to spend, primarily due to tax-related uncertainties. Among those under $50,000 household income, 57% avoid spending; this rises to 67% for $50,000–$99,999 earners and peaks at 78% for those over $100,000.

Absent an opt-out choice, eligible parents have commenced receiving these installments, prompting varied responses on fund allocation. Thirty-eight percent plan to save the amounts, 35% intend to settle bills, 28% aim to invest for their children’s future, and 27% will direct funds toward essential family or child-related needs.

Although optimism tempers consumer sentiment regarding economic prospects and outlays, a prevalent observation among buyers is the diminished purchasing power of their dollars. Eighty percent of survey participants feel their money stretches less than before. Correspondingly, three-quarters note price hikes in routine purchases over the recent three-month span.

In response to eroding dollar value, shoppers are adapting their procurement strategies. The predominant countermeasure is hunting for discounts or promo codes prior to buying (38%). About one-third (32%) report reducing purchase volumes due to cost increases, while 29% postpone acquisitions owing to inflated pricing.

Nowhere is the surge in prices more disruptive than in residential real estate. Elevated demand coupled with constrained inventory in numerous locales has intensified competition. Data from this quarter’s study indicates that 60% of recent homebuyers (within the last three months) disbursed sums exceeding the asking price. For prospective buyers, these conditions breed substantial worry: 80% fear inability to compete in their overheated local markets, and 75% dread failing to secure properties within budgetary limits.

These pressures disproportionately affect upper-income segments. Among households over $100,000, 70% of recent buyers paid above list price, versus 56% in the $50,000–$99,999 range and 37% below $50,000. Likewise, high earners (83%) outpace others (71%) in concerns over budget feasibility for upcoming purchases.

Perhaps most alarmingly, competitive fervor drives risky concessions: 75% of near-term buyers are open to forgoing inspections and appraisals to strengthen bids. Such shortcuts for immediate advantage expose purchasers to prolonged vulnerabilities amid this summer’s rigorous market dynamics.

Quarter 2 findings highlight burgeoning interest in novel investment avenues, such as cryptocurrencies and automated advisory services, particularly among younger demographics. Sixteen percent of active investors have ventured into crypto assets. Millennials lead adoption at 27%, surpassing Gen X at 15% and Boomers at a mere 5%.

Millennials also favor digital platforms: 51% utilize apps like Robinhood, compared to 32% of Gen X and 5% of Boomers. Robo-advisors follow suit, with 44% of Millennials engaged versus 22% Gen X and 4% Boomers.

This affinity for self-directed tools likely reflects Millennials’ elevated investment self-assurance: 51% rate themselves as extremely confident, dwarfing Gen X (32%) and Boomers (11%).

From orchestrating large acquisitions and calibrating post-pandemic spending caution to navigating child tax credit usage, fiscal choices challenge wedded pairs lacking financial alignment.

Forty-one percent of married respondents report recurrent spousal conflicts during money talks. Additionally, 37% feel guilt-induced by partners over spending habits, with Millennials hit hardest (65%), followed by Gen X (41%) and Boomers (11%).

Beyond disputes, secrecy prevails: one-third admit concealing spousal-disapproved purchases. Further, 31% maintain undisclosed credit cards, and another 31% hidden debts.

Debt exacerbates tensions: 54% of indebted couples frequently argue over finances (versus 25% debt-free), and they are twice as prone (50% vs. 23%) to spousal guilt-tripping on expenditures.

With 37% noting improved personal finances year-over-year (against 18% reporting declines), a positive trajectory emerges as the year progresses into its latter half. Nonetheless, as Q2 metrics underscore, citizens grapple with evolving fiscal pressures encompassing child tax credits, inflationary squeezes, real estate hurdles, and persistent spending wariness.

Ramsey Solutions’ State of Personal Finance Study constitutes a quarterly survey involving 1,004 U.S. adults, designed to illuminate prevailing personal finance practices and mindsets nationwide. The representative sample was gathered from June 22 to June 29, 2021, via an independent research panel.