Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

Inflation occurs when the prices of goods and services steadily increase over time, resulting in a reduction of your money’s purchasing power. This economic phenomenon is influenced by various drivers such as heightened demand for products, escalating production expenses, and anticipations of future price hikes. The Federal Reserve plays a crucial role in controlling inflation through adjustments to interest rates and by monitoring essential indicators like the Consumer Price Index (CPI). Individuals can safeguard their finances against inflation by creating a monthly budget, saving strategically, and pursuing investments aimed at long-term objectives.

Many of us have listened to grandparents or parents fondly recall the affordability of life in previous eras, sharing stories like these nostalgic memories highlight how dramatically costs have changed.

Inflation refers to the sustained rise in the prices of goods and services across an economy over a period. As these prices climb, the purchasing power of your currency diminishes significantly. For instance, half a century ago, five dollars could fully refuel your vehicle, but today, that same amount barely registers on the gauge.

The inflation rate frequently mentioned in media reports represents a percentage reflecting the year-over-year change in price levels. An inflation rate of 10%, for example, indicates that prices have risen by 10% compared to the previous year. In practical terms, this translates to a shopping basket costing $100 last year now requiring approximately $110.

This concept is far from novel, though recent discussions have intensified due to elevated levels not witnessed in decades, leading to noticeable strain from surging costs at fuel stations and supermarkets.

In September 2025, the U.S. inflation rate for the preceding 12 months stood at 3%. This marks a substantial decline from the peak of 9.1% recorded in June 2022, which was the highest in four decades. While there has been some easing over the past year, the rate remains elevated beyond the 2% threshold considered optimal by many economic experts for sustainable growth.

Inflation arises when the cost of goods and services escalates while the value of currency erodes progressively. At its core, this ties directly to the principles of supply and demand. When consumer desire for products outpaces availability, sellers naturally raise prices to balance the market.

Economists identify three primary categories of inflation, each characterized by distinct mechanisms that propel price increases. Let’s examine these in detail.

Demand-pull inflation emerges when the demand for goods and services surges beyond the available supply, effectively pulling prices upward. This scenario often stems from consumers possessing excess funds relative to the quantity of goods on offer—a condition economists term as too much money pursuing limited products.

Such surplus liquidity might originate from a robust employment landscape with low unemployment, enabling higher earnings. Alternatively, it could result from accessible credit amid low interest rates or direct government interventions like stimulus payments. A thriving economy further bolsters consumer confidence, encouraging spending and borrowing over cautious saving for unforeseen needs. Substantial government expenditures, given its massive buying power, can also contribute to upward price pressure.

Cost-push inflation occurs when the expenses associated with raw materials and production inputs rise for manufacturers. These increased costs are then passed along to consumers, pushing retail prices higher, often triggered by supply disruptions. A prime example unfolded during the 2020 COVID-19 crisis, where global supply chains faltered and factories halted operations. While some spikes arose from panic purchasing, production stoppages were the primary culprits. Energy resources like oil frequently factor in, given their integral role in transportation, manufacturing, and countless products; oil price surges ripple through the broader economy.

Built-in inflation presents a self-perpetuating cycle where prior inflationary pressures breed expectations of ongoing rises. Once demand-pull or cost-push forces elevate prices, workers anticipate continued increases, prompting demands for salary hikes or job switches to higher-paying roles. Businesses respond with cost-of-living adjustments to retain staff. These wage escalations, in turn, fuel further price increments, forming what is known as the wage-price spiral—a feedback loop sustaining inflation.

Fundamentally, inflation stems from supply-demand imbalances. Scarcity of essential or desirable items fosters competition, driving costs up and instilling a sense of urgency among buyers. Conversely, excess production beyond demand leads to price reductions.

Consider a straightforward illustration: If an automaker produces 10,000 units of a model but only 9,000 buyers exist at the prevailing price, surplus inventory necessitates discounts to clear stock. Should demand reach 11,000, the manufacturer can elevate prices until equilibrium aligns supply with willing purchasers.

Real-world pricing involves far greater complexity, with businesses forecasting demand amid uncertainties. Inflation materializes not from isolated instances but widespread price adjustments across sectors. Its effects rapidly permeate retail outlets and household budgets. For context, grocery prices have climbed 3% over the past year, making everyday staples noticeably pricier and challenging prior spending norms.

Inflation persists despite earlier assurances from policymakers in 2021 labeling it temporary. Current trends indicate ongoing challenges ahead.

Transitory inflation describes short-term price elevations that subside without enduring impact. This term applies to fleeting spikes that peak briefly before reverting, implying minimal long-term disruption.

Recent experiences deviate sharply from this pattern, with persistent pressures demanding adaptive strategies rather than passive expectation of decline.

In the United States, inflation tracking relies on three core metrics: the Consumer Price Index (CPI), Producer Price Index (PPI), and Personal Consumption Expenditures Price Index (PCE). These tools meticulously monitor price fluctuations in consumer goods, production inputs, and actual expenditures.

Among them, the CPI garners the most attention from analysts due to its direct relevance to household experiences.

The CPI quantifies shifts in the costs of a representative basket of goods and services purchased by typical households. It compares current pricing against prior periods, such as monthly or annual benchmarks, encompassing essentials from toiletries to housing.

The PPI parallels the CPI but focuses on revenues received by producers for their outputs, capturing wholesale-level changes across roughly 500 sectors. Unlike CPI, it excludes consumer-end factors like taxes, subsidies, and retail markups, offering an upstream perspective on inflationary trends.

The PCE tracks real-world price variations for services and goods based on verified consumer transactions, providing insights into spending behaviors and their inflationary implications.

Analyzing these indexes, though data-intensive, yields comprehensive views of economic pressures and currency valuation shifts.

Purchasing power encapsulates the real-world utility of money—essentially, how much one can acquire with a given sum. A dollar’s capacity to procure goods has steadily waned over decades. Recent surveys reveal nearly half of Americans struggle with bill payments, underscoring inflation’s tangible bite on daily finances.

Economic literature distinguishes several inflation variants, each with unique characteristics and consequences.

Deflation manifests as declining prices and negative inflation rates below zero percent. This enhances short-term purchasing power, allowing more value per dollar spent. However, prolonged deflation hampers growth, stagnates wages, and elevates unemployment risks, making it undesirable despite surface appeal.

Stagflation combines sluggish or halted economic expansion, elevated unemployment, and relentless price increases occurring simultaneously. The U.S. last endured this in the 1970s, raising concerns of potential recurrence absent corrective measures.

Hyperinflation represents runaway price surges, conventionally defined as monthly increases exceeding 50%. Everyday items like milk could double or triple in cost within months, eroding savings catastrophically. Historical precedents, such as post-World War I Germany, saw citizens hauling cash by the cartload for basics—rare but devastating when it strikes.

Shrinkflation subtly erodes value by reducing product quantities while maintaining prices, shielding corporate margins amid inflationary strains. Shoppers notice familiar packages yielding less content, such as a candy bag shrinking from 12 to 10 ounces at unchanged cost—a covert adjustment masquerading as stability.

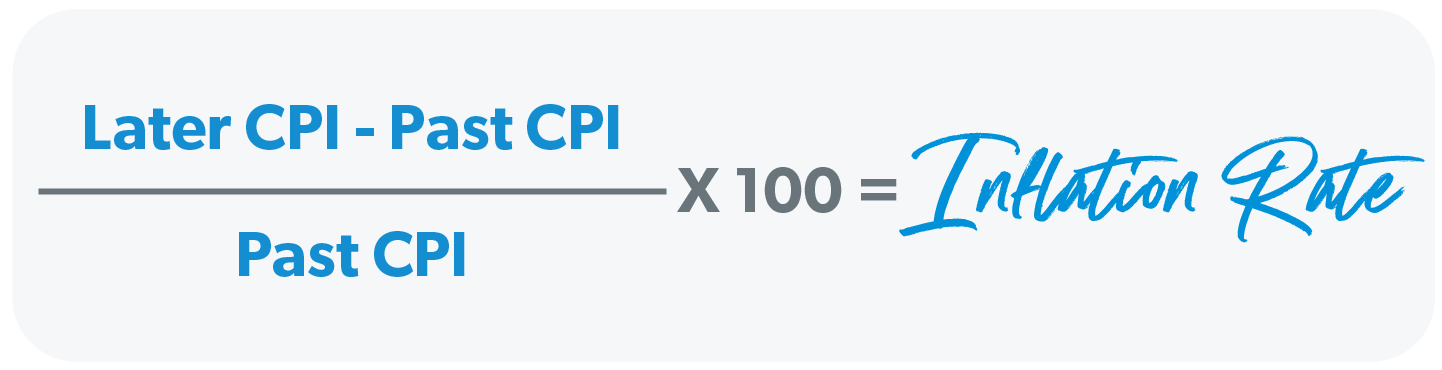

Determining precise inflation requires referencing the CPI alongside a straightforward formula. Though initially intimidating, application clarifies its utility.

To illustrate, suppose gasoline priced at $1.55 per gallon in 2000 rose to $2.25 by 2020. Subtract the initial price from the final: $2.25 minus $1.55 equals $0.70. Divide by the base price: $0.70 divided by $1.55 approximates 0.45. Multiply by 100 for a 45% inflation rate over that span.

Official tools from the Bureau of Labor Statistics enable further explorations, revealing equivalences like $1 from 1951 matching $12.39 today—dramatizing erosion across generations.

Low interest rates, as seen in 2020 for mortgages, stimulate borrowing and spending, fostering growth but risking price acceleration. Elevated rates conversely curb consumption, decelerate expansion, and theoretically temper inflation by incentivizing saving over expenditure.

Higher home loan rates deter buyers, while improved returns on savings encourage accumulation. The Federal Reserve orchestrates this via the federal funds rate, influencing broader lending from bonds to consumer credit, targeting a 2% CPI equilibrium.

Far from inevitable doom, proactive steps empower individuals to mitigate inflation’s reach effectively.

Amid hype, resist impulses like hoarding fuel, precious metals, or staples. Preparation thrives on rationality—steady nerves form the foundation.

A zero-based budget assigns every dollar purposefully, spotlighting trim opportunities without sacrificing essentials. Rising local costs for fuel or food necessitate recalibrations, ensuring alignment with realities like bread jumping from $2 to $3 per loaf.

Scan for pauses in discretionary outlays, such as vacations or extracurriculars, redirecting funds to strained categories like dairy.

Target efficiencies in groceries through home cooking, generic substitutions, or carpooling. Stock budgeted pantries with non-perishables during promotions, averting wasteful panic acquisitions reminiscent of early pandemic shortages.

Long-term horizons guarantee costlier necessities; counter this via diversified investing post-debt clearance (excluding mortgages) and emergency reserves. Early action compounds protections against inevitable rises.

Mastering inflation demands informed planning beyond mattress hoards. Engaging seasoned financial professionals crafts tailored investment blueprints, maximizing resilience through insightful, personalized counsel.