Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

Unlike the majority of homeowners, I have a strong preference for adjustable-rate mortgages, commonly known as ARMs. These financial instruments have enabled me to avoid more than $300,000 in mortgage interest costs since 2005, in stark contrast to what I would have paid with traditional 30-year fixed-rate loans.

Even amid widespread apprehension, uncertainty, and skepticism about ARMs, they have proven to be among the most effective strategies for accumulating wealth in my personal financial journey. By capitalizing on attractive initial rates and directing surplus funds toward principal reduction whenever possible, I have steadily minimized interest expenses while preserving significant operational flexibility.

In this detailed analysis, I present a practical, real-life example that directly confronts one of the primary concerns associated with ARMs: the scenario where interest rates surge substantially after the initial fixed period concludes. In such a case, does the borrower end up suffering financially and wishing they had opted for a stable 30-year fixed-rate mortgage instead?

I firmly believe that a substantial portion of the apprehension, worry, and even outright opposition stems from a lack of comprehensive knowledge about the intricacies involved. The deeper our comprehension of a topic—or even of another individual—the less space remains for unfounded fears or animosity.

With that perspective in mind, let us dive into the details, addressing this topic with clear-eyed openness.

Unfortunately, a 7/1 ARM that I originated in December 2019 is approaching its reset date in December 2026.

During 2019, I refinanced the maturing balance of $700,711 from my previous 5/1 ARM, which carried a 2.5 percent rate, into this new 7/1 ARM at 2.625 percent. At that juncture, securing a 30-year fixed-rate mortgage was feasible at approximately 3.375 percent. Nevertheless, the substantial gap between the ARM rate and the fixed option did not justify the switch. Moreover, I was certain that I would not hold onto the mortgage for even a fraction of 30 years. This property, acquired in 2014 as a fixer-upper, accommodated a family of three comfortably but proved less suitable once our family expanded to four members.

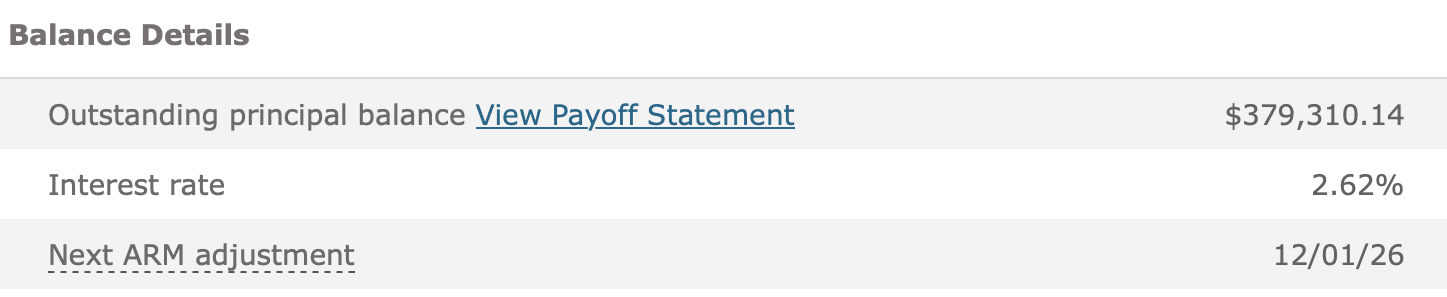

Today, the outstanding mortgage balance has dwindled to about $379,000, representing a 45 percent reduction from the 2019 refinance amount and a whopping $615,000 drop from the 2014 purchase price. Honestly, I anticipated an even lower balance by this point. However, the onset of the COVID-19 pandemic in 2020 prompted me to pause extra principal payments, redirecting those funds instead to capitalize on market downturns in various risk assets.

That strategic pivot yielded impressive financial returns, though it consequently slowed the pace of mortgage principal amortization compared to my original projections.

Coincidentally, I lack the $360,000 in liquid cash required to eliminate the mortgage prior to its December 2026 reset. Portions of my available capital—around $100,000—are already committed to capital calls in private closed-end investment funds. Additionally, I intend to sustain dollar-cost averaging into publicly traded equities and allocate at least another $50,000 toward venture opportunities for my children this year.

Thus, this situation mirrors the challenge confronting numerous ARM holders in the coming years: How should one handle an expiring ARM when prevailing interest rates have climbed significantly higher than at origination?

When an adjustable-rate mortgage nears the conclusion of its introductory fixed-rate phase, borrowers essentially face three primary pathways forward.

Personally, I am eager to avoid the hassle of another mortgage application or refinancing process if at all possible, making refinancing the least appealing choice. Liquidating assets to settle the mortgage outright would incur unwelcome capital gains taxes that I prefer to sidestep.

This narrows my viable alternatives to gradual payoff or permitting the adjustment while adeptly managing the elevated rate and corresponding payments.

Upon thorough number-crunching, permitting the ARM to reset emerges as the most rational course of action. In fact, I contend that this represents the optimal strategy for the vast majority of individuals grappling with a comparable predicament.

A frequently overlooked feature of adjustable-rate mortgages pertains to the mechanics governing rate escalations.

Prior to finalizing any plan, I consulted my mortgage officer to verify the precise rate limitations embedded in my loan agreement. This ARM incorporates both an annual adjustment ceiling and an overall lifetime maximum rate.

The initial reset permits a maximum uptick of 2 percentage points. The absolute ceiling for the loan’s duration caps at 7.65 percent.

In the most adverse circumstances, this translates to my rate climbing from 2.65 percent to 4.65 percent starting in December 2026, holding steady for the subsequent 12 months. Remarkably, even at 4.65 percent, this remains approximately 1.35 percentage points below the current average for 30-year fixed-rate mortgages, which hover around 6 percent.

Faced with these parameters, the prudent approach is to allow the adjustment to occur and then reevaluate conditions after the first year elapses.

Following that inaugural adjustment, subsequent annual changes remain constrained by the 2 percent yearly cap. Should mortgage rates persist at elevated levels or climb further, the rate could theoretically reach 6.65 percent by the ninth year of the loan term, corresponding to the second post-adjustment year.

From a historical vantage point, 6.65 percent aligns closely with the longstanding average for U.S. mortgage rates and does not constitute an exorbitant burden. That said, I anticipate the second-year increment might fall short of the full 2 percent limit.

Assuming mortgage rates stabilize at present levels, the year-nine adjustment might approximate just 1.5 percentage points, elevating the rate to around 6.15 percent. Should rates soften, the rise could prove even more modest.

The crucial insight here is the absence of any pressing need for immediate action. Deferring decisions until the conclusion of the first adjustment period affords superior insights and greater adaptability.

Beyond fixating on the interest rate adjustment itself, the paramount consideration for an impending ARM reset involves scrutinizing the ensuing monthly payment obligation.

To illustrate, consider these foundational assumptions for my scenario. The loan originated as a $700,711 7/1 ARM, amortized over 30 years in December 2019. Upon resetting in December 2026, precisely 23 years—or 276 months—will remain on the term.

Currently, my $2,814 monthly payment allocates roughly $1,984 to principal reduction and $830 to interest accrual.

Post-reset, the recalculated monthly payment drops to approximately $2,238—a substantial $576 reduction from the original $2,814 figure at loan inception. This counterintuitive outcome arises from my aggressive 45 percent principal paydown over the initial seven years.

Breaking down the first post-reset month’s $2,238 payment, fixed for one year, reveals the following composition:

Psychologically, observing a larger interest allocation and diminished principal progress can feel disheartening on a monthly basis. Yet, prioritizing the overarching financial narrative outweighs these superficial monthly impressions.

Despite a 2 percentage point rate surge, the monthly payment still contracts meaningfully from $2,814 to $2,238.

With the balance now under $400,000, the inherent risks of an ARM reset are effectively mitigated.

Should rates ascend another 2 points in year nine—the second adjustment year—factoring in standard amortization, the payment might climb to about $2,665, with roughly $2,050 directed to interest. While suboptimal, this remains entirely manageable, staying $149 below the original seven-year payment of $2,814.

This exemplifies how diligent early principal reductions transform potential rate volatility into a negligible concern.

A 4.65 percent mortgage rate qualifies as competitively low on an absolute basis. However, it now surpasses the risk-free benchmark, exemplified by the 10-year Treasury yield.

Once the mortgage rate eclipses this risk-free threshold, the decision calculus simplifies considerably.

Funds earmarked for U.S. Treasuries become better directed toward mortgage principal, as a assured 4.65 percent yield trumps a 4.2 percent Treasury return, for instance. Naturally, one must account for liquidity requirements, since accessing home equity can entail added expenses.

Leveraging the $576 monthly payment reduction post-reset, I intend to maintain payments at the prior $2,814 level during the initial adjustment year. This strategy channels the full $576 surplus directly to principal without disrupting cash flow.

Furthermore, given the mortgage rate’s edge over the risk-free alternative, I plan to allocate an extra $20,000 toward principal that year—equivalent to what might otherwise flow into Treasuries.

Prior to the first adjustment year’s close, I will revisit this comprehensive evaluation, incorporating fresh rates, balances, and opportunity costs. Every ARM holder in a similar position should follow suit.

Having meticulously worked through this framework, I advocate that most ARM borrowers confronting elevated rates seriously contemplate allowing the reset while persisting with targeted extra principal payments.

This methodology curtails unnecessary complications, bypasses refinancing fees, sustains adaptability, and frequently yields the minimal cumulative interest outlay. The inaugural year under the new rate may well undercut prevailing mortgage offerings substantially.

Refinancing holds merit only if rates plummet appreciably. The process typically spans 30 to 60 days, demands voluminous documentation, and incurs fees of 1 to 2 percent of the loan amount—a burdensome endeavor for many.

Thus, I would pursue refinancing solely if the breakeven timeline spans 18 months or fewer. Given that the typical homeownership duration averages 12 to 13 years, numerous owners inadvertently inflate their projected tenure from a refinance.

Post-introductory ARM phase, pragmatic assessments eclipse theoretical ideals. Assuming a 30-year fixed mortgage at a premium rate based on an overestimated 17- to 18-year hold undermines financial efficiency.

In essence, I welcome the 2 percent reset on my ARM, especially as it coincides with a $576 monthly payment decline.

This dynamic gains added significance since I recently augmented rental revenue from this property by $3,500 monthly. This followed leasing the entire home at current market rates after a tenant transition. Previously, only the upstairs unit generated income, with the same occupant from late 2019 through mid-2025.

Consequently, this single property now contributes an extra $48,912 annually to my semi-passive income stream, offsetting the rate increase handily.

I acquired the property in 2014, residing there for six years post-renovations. It provided an ideal residence during the early years with my wife, and after our son’s 2017 arrival. The asset has appreciated solidly and now anchors our retirement income portfolio.

Securing an ARM facilitated the initial purchase. Retaining it sustains affordable payments and flexibility until payoff.

My objective remains full payoff by 2030—16 years from acquisition. Achieving this demands approximately $50,000 in supplemental annual principal reductions over the next five years. With a detailed roadmap in place, success feels assured.

Were I a first-time buyer or eyeing another long-term residence today, I would unequivocally pursue a 7/1 or 10/1 ARM anew. Over seven to ten years, at minimum 15 percent principal amortization occurs, alongside a solid probability of relocation or sale pre-reset.

A 30-year fixed mortgage undoubtedly confers tranquility, but realistic life modeling often reveals ARMs delivering superior savings, versatility, and command.