Not Sure Where To Start?

One question. Seven possible paths. Find the right articles for your financial situation in seconds.

A widespread notion persists within the investment community that generating alpha—essentially outperforming the broader market—represents the ultimate goal for any serious investor. This perspective makes complete sense on the surface. Assuming all other factors remain constant, achieving higher levels of alpha will invariably deliver superior outcomes compared to lower levels.

Nevertheless, possessing alpha does not guarantee superior investment performance in every situation. The key reason lies in the fact that alpha is inherently measured in relation to the market’s overall performance. Should the market experience a downturn or stagnation, even substantial alpha may fail to prevent disappointing results. To clarify this concept, consider a straightforward illustrative scenario involving two hypothetical investors.

Picture Alex, a highly competent investor who consistently surpasses the market by 5 percentage points annually. In contrast, meet Pat, an inept investor who regularly trails the market by the same 5 percentage points each year. If both began their investment journeys simultaneously, Alex would reliably eclipse Pat by a full 10 percentage points per year, highlighting the clear advantage of skill in a side-by-side comparison.

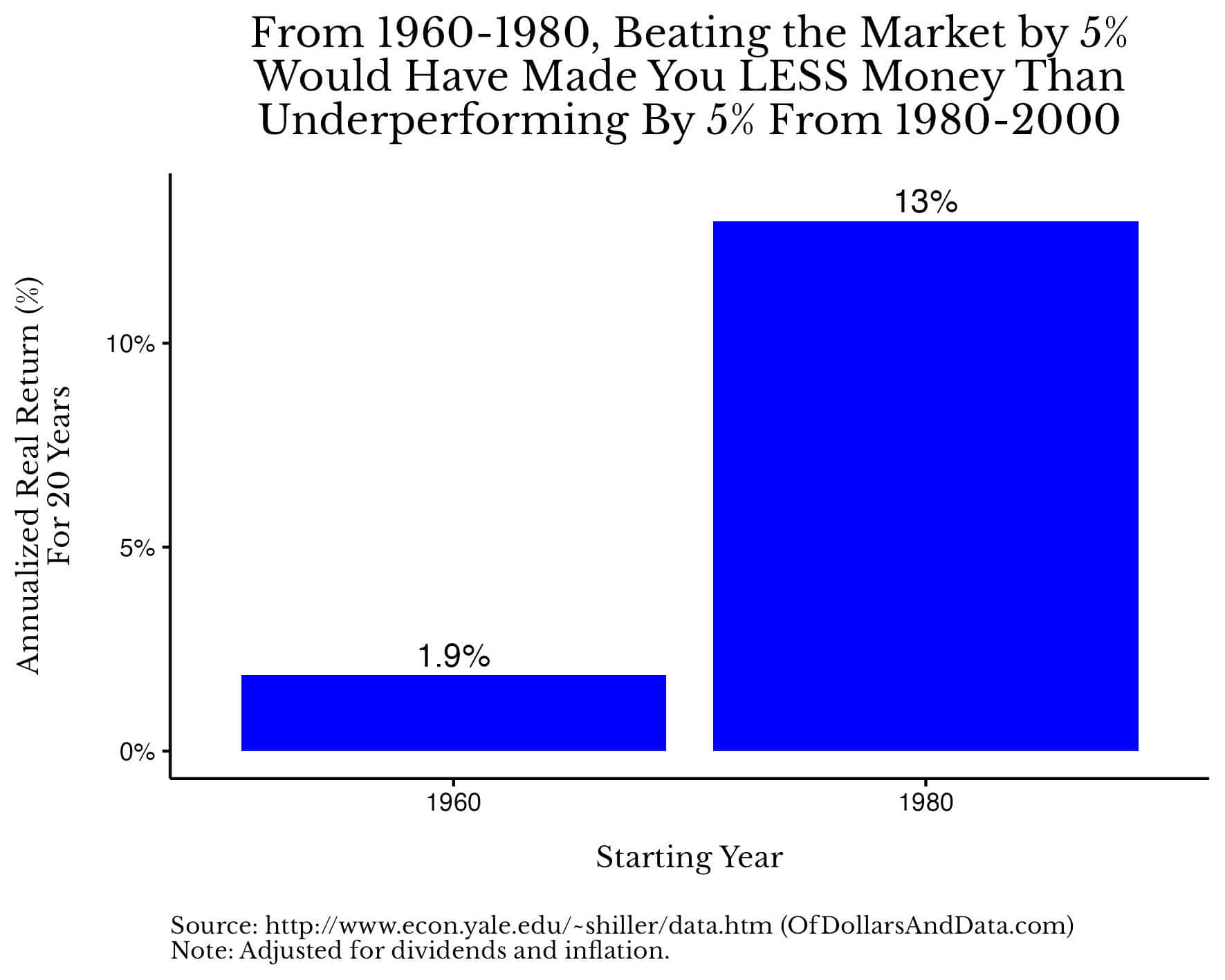

Now, introduce a twist: what happens if Pat commences investing at a markedly different time from Alex? Could there exist circumstances where the less skilled Pat actually achieves better long-term results than the talented Alex? The answer is a resounding yes. For instance, suppose Alex poured money into U.S. stocks from 1960 through 1980, while Pat entered the market from 1980 to 2000. After two decades, it would be Pat who emerges with the higher total return, despite Alex’s evident superiority.

This counterintuitive outcome stems from the dramatically divergent market conditions across those periods. The weaker market environment during Alex’s tenure drags down even skilled performance, whereas Pat benefits from a robust bull market that more than compensates for their shortcomings.

To push this further, let’s pit Alex against a more realistic adversary—not the underperforming Pat, but a passive index investor who simply mirrors the market’s returns year after year without deviation. Even in this matchup, Alex, generating a 5% alpha premium, would still lag behind the index investor if starting in 1960 and comparing to an indexer beginning in 1980. This underscores how extreme timing differences can override even significant skill advantages.

While the above represents an outlier case, it reveals a broader truth about the limitations of alpha. Historical data reveals that alpha generation frequently results in underperformance when benchmarked against passive indexing over extended horizons. Analyze the frequency with which various levels of alpha fail to beat an index across every possible 20-year window in U.S. stock market history from 1871 through 2025.

The visualization clearly demonstrates that zero-alpha investors—those matching the market exactly—face roughly a 50% chance of underperforming an indexer over any given 20-year span, akin to a coin toss. As alpha rises, the odds of underperformance decline, yet the improvement is less dramatic than intuition might suggest. Remarkably, an investor generating a consistent 3% annualized alpha still encounters a 25% probability of trailing a passive indexer in certain historical periods. This highlights the persistent risk introduced by market timing variability.

Some proponents of active management insist that relative performance is the sole metric of importance, dismissing absolute returns. However, this view overlooks critical realities. Would any rational investor prefer matching the market during prosperous eras or merely losing less than peers—thereby generating positive alpha—amid catastrophes like the Great Depression? The unequivocal choice favors capturing full market returns in favorable times, as these compound into substantial wealth creation over the long haul.

Historical evidence supports this preference emphatically. U.S. stocks have delivered positive real annualized returns across most decades since 1900, with variations but few prolonged slumps. Note that the 2020s data reflects outcomes only through 2025.

These patterns affirm that while individual investor skill undoubtedly influences outcomes, the overarching market trajectory—beta—exerts a far more dominant force. In essence, investors would do well to wish for strong beta exposure rather than chasing elusive alpha.

In technical terms, beta quantifies an asset’s sensitivity to market movements. A beta of 1 indicates returns move in lockstep with the market, while higher or lower values amplify or dampen those swings accordingly. For the purposes of this discussion, beta simply denotes capturing the market return itself.

Fortunately, market cycles exhibit mean-reverting tendencies, meaning periods of subdued beta are often followed by robust recoveries. This dynamic is vividly captured in the rolling 20-year real annualized returns of U.S. stocks spanning 1871 to 2025.

Observe the sharp rebounds following troughs. An investment launched in 1900 yielded nearly 0% real annualized return over the ensuing two decades, marred by early 20th-century turmoil. Shift forward to 1910, and the same horizon delivers approximately 7%. Late 1929 entrants endured about 1% amid the Depression, while mid-1932 investors reaped 10%. Such swings emphasize beta’s outsized role relative to alpha in determining final wealth.

You might wonder, given the uncontrollability of market beta, why dwell on this? The insight proves liberating precisely because it redirects energy toward controllable elements of personal finance and life. Rather than agonizing over unpredictable market forces, embrace them as one fewer burden. This mindset eliminates the futile pursuit of timing or outguessing the market.

Redirect that focus to domains within your grasp: advancing your professional trajectory, maximizing savings contributions, maintaining physical well-being, nurturing family relationships, and beyond. These levers generate exponentially greater lifetime value than marginal portfolio outperformance.

The cumulative impact of these choices dwarfs the gains from active stock-picking or market-beating strategies, which elude even professionals. Embrace this clarity as you plan for 2026 and beyond: cultivate what you control, then hope for favorable market beta to amplify your efforts.